Last updated: April 2026

A few weeks ago I got curious about who still writes checks. The headlines all said paper checks were dying. My own kid didn't even know what a checkbook was. So I went and looked.

The number that fell out of the data shocked me. Americans still write about 11 billion paper checks a year, moving $27.4 trillion in total value. That's nearly three times the dollar value of every US credit and debit card transaction combined ($9.6 trillion).

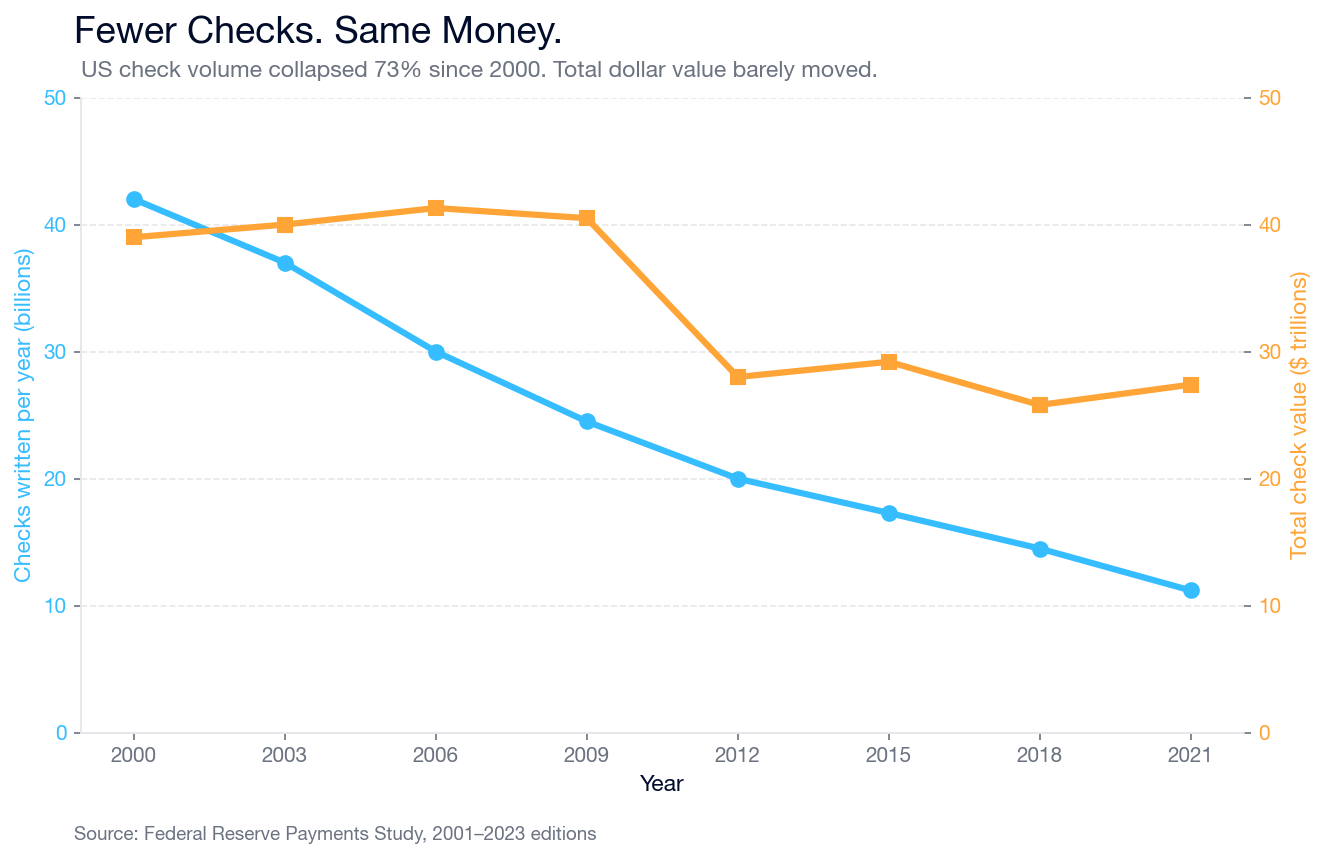

Yes, check volume is collapsing. Down 73% since 2000. But the total dollars moving through checks? Basically flat. Fewer checks. Same money.

TL;DR:

- Federal paper checks are ending (IRS refunds, Social Security)

- Private-sector paper checks are not. Small businesses still push $27 trillion a year through them

- The industries still using checks are specific: staffing, medical, churches, contractors, nonprofits, trucking, law firms

- I run CheckDeposit.io, a free deposit-slip tool. 81,000 slips from 38,000 businesses tell me exactly who the holdouts are, and why they're not switching

Here's the whole story: what's changing, what isn't, and why the check you got in the mail last week isn't going away anytime soon.

What's Actually Changing (and What Isn't)

The federal government is ending paper checks. That part is real.

Executive Order 14247, signed on March 25, 2025, took effect September 30, 2025. It directs the Treasury and the IRS to phase out paper checks for federal payments. That covers IRS tax refunds, Social Security benefits, VA payments, vendor payments to federal contractors, and most other money the government sends out. It also gradually phases out paper checks going IN to the government (tax payments, fees, penalties).

The federal government had already mostly moved to electronic. Only 7% of IRS refunds were still mailed as paper checks by the 2025 tax season. By fiscal year 2023, 96.45% of Treasury disbursements were already electronic funds transfers. The executive order is finishing a job that's been underway for a decade.

What the order does NOT cover: the check your customer hands you at the counter. The check your insurance company mails after a hailstorm. The tithe check in the offering plate on Sunday morning. The check your staffing agency's client cut for last month's invoice.

Nothing in EO 14247 changes whether your bank accepts paper check deposits (it does, and will), whether you can pay vendors by check (you can), or whether your customers can pay you by check (they can).

If you're a small business owner trying to figure out if this affects you, the short answer is: probably only at tax time.

The Fed Paradox: Fewer Checks, Same Money

The Federal Reserve Payments Study is the gold-standard dataset for how Americans pay each other. It's published every three years. The 2022 edition (released in 2023, covering 2021 data) is the most recent. It's where the "checks are dying" narrative comes from, and it's also where the counter-story lives.

Start with the headline narrative. Here's the Fed's count of paper checks written in the US, back to the turn of the century:

| Year | Checks written (per year) |

|---|---|

| 2000 | ~42 billion |

| 2012 | ~20 billion |

| 2015 | ~17 billion |

| 2018 | 14.5 billion |

| 2021 | 11.2 billion |

From 2018 to 2021 alone, check count dropped 7.2% per year. That is a steep, consistent decline. By that measure, yes, paper checks are going away.

Now the same Fed study's figures for the total dollar value carried by those checks, same years:

| Year | Total check value |

|---|---|

| 2015 | ~$29 trillion |

| 2018 | ~$25.8 trillion |

| 2021 | $27.4 trillion |

Basically flat. The total money moving through paper checks has fluctuated between $25 and $29 trillion a year for most of that stretch. In 2021 it ticked up, growing at 0.6% a year from 2018 even as check count fell 7.2% a year.

Let that sink in for a second. The number of checks is crashing. The dollar volume is not. To put $27.4 trillion in context: US credit and debit cards combined moved about $9.6 trillion in 2021 (per the same Fed study). Paper checks moved nearly three times that.

How does the check count crash while the dollar value holds steady? Average check size. Per the Fed, that line has gone straight up for 20 years:

| Year | Average check |

|---|---|

| 2000 | $945 |

| 2003 | $1,103 |

| 2012 | $1,410 |

| 2018 | $1,908 |

| 2021 | $2,430 |

Checks have more than doubled in average size since 2000 while shrinking to about a quarter of their old volume. The average 2021 check is worth about $2,430. The typical debit card transaction, by comparison, is around $45 (per the same Fed study).

The pattern is consistent for a simple reason. Casual users, the grocery-store-checkbook crowd, have mostly left. Business users writing high-value invoice and settlement checks have not. What's left in the American check system is fewer transactions, each doing more work. It is not a dying payment method. It is a specializing one.

The Fed tells us WHAT is happening at the national level. It does not tell us WHO. For that, we turned to our own data.

Our Zoom-In: What We Saw in 81,529 Deposit Slips

We started CheckDeposit.io in 2019 as a free tool. No signup. No ads. No catch. Type in a routing number, fill in four fields, print a perfect deposit slip for any US bank. 38,000 businesses have used it.

Here's what the numbers look like, end to end:

- Total slips printed: 81,529

- Total check value processed: about $1 billion (filtered for obvious data-entry errors)

- Average checks per deposit: 3

- Median check size: about $400

- Years of data: 7

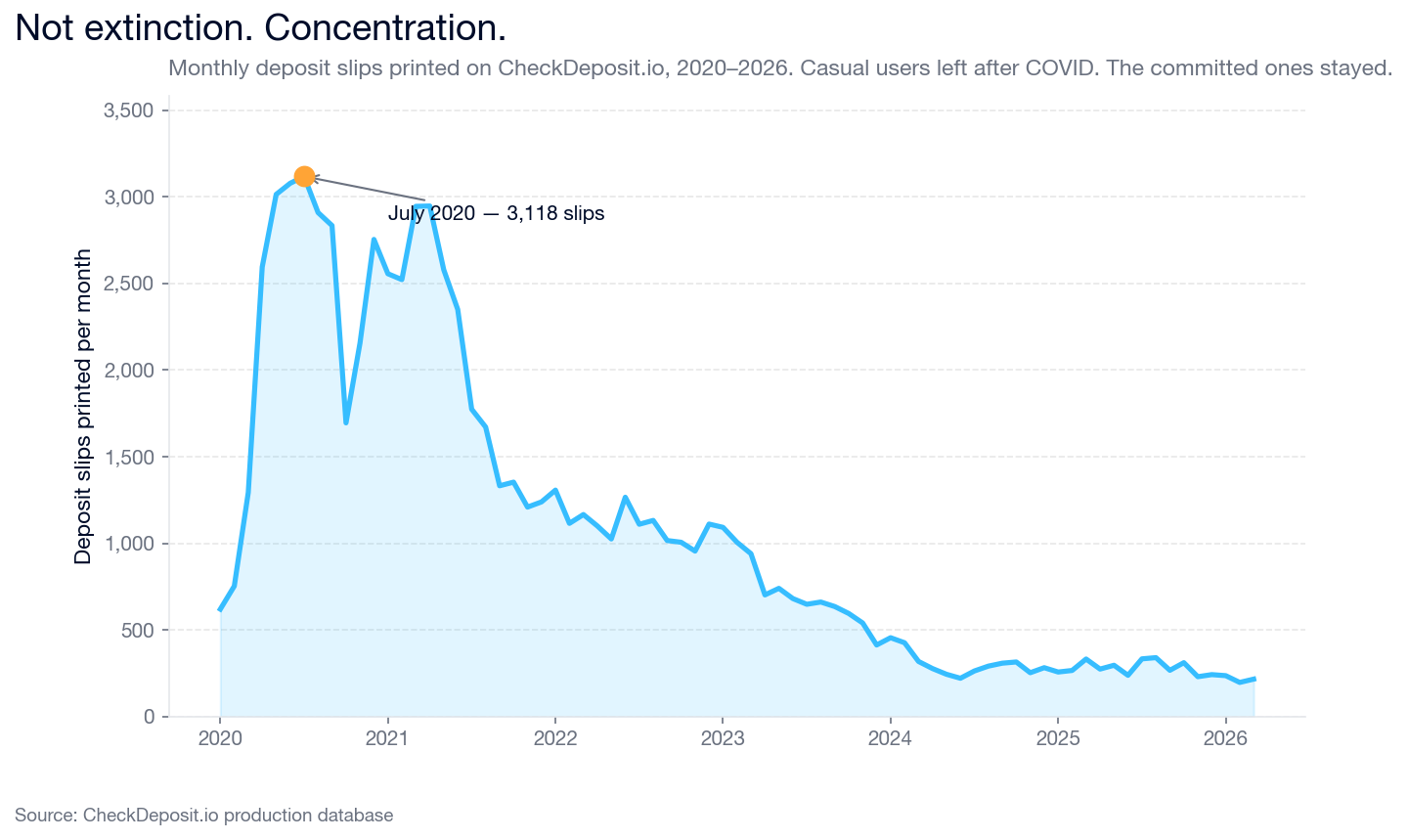

The trend over time is where it gets interesting. 2020 was the peak: 26,818 slips, driven by PPP checks, pandemic stimulus, and a general scramble to move money. Then a long decay. 13,000 slips in 2022. 8,700 in 2023. 3,700 in 2024. In 2025 we printed 3,386 slips. So far in 2026, we're on pace for about 2,600.

Honest caveat before you get too impressed with that chart: our site traffic cratered just as hard over the same years. So some of what you're seeing is probably "fewer people finding CheckDeposit," not purely "fewer people depositing checks." We'd rather say that out loud than pretend we're bigger than we are.

That said, the shape of our decline tracks the Fed's national numbers (volume down, a long decay, a stable floor). It also lines up with what we see when we look at the businesses who stayed. Which brings us to the interesting part: the ones who never left.

It isn't extinction. It's concentration. The casual users, the ones who needed one emergency deposit slip in March 2020, never came back. The committed users kept printing.

Look at the distribution of how many times individual businesses have used our tool:

- 74.2% of businesses printed exactly one slip and never returned

- 23.6% came back for 2 to 5 slips

- 1.4% printed 6 to 12 slips

- 0.7% printed 13 to 52 slips (a near-weekly cadence)

- 0.1% (44 businesses) printed more than 52 slips each

The hard-core 44 are a mix we did not expect: orthodontics practices, national nonprofits, staffing agencies, martial arts schools, chiropractors, law firms, trucking companies, a water-treatment company, and yes, a bankers' association.

Who Still Uses Checks in 2026 (By Industry)

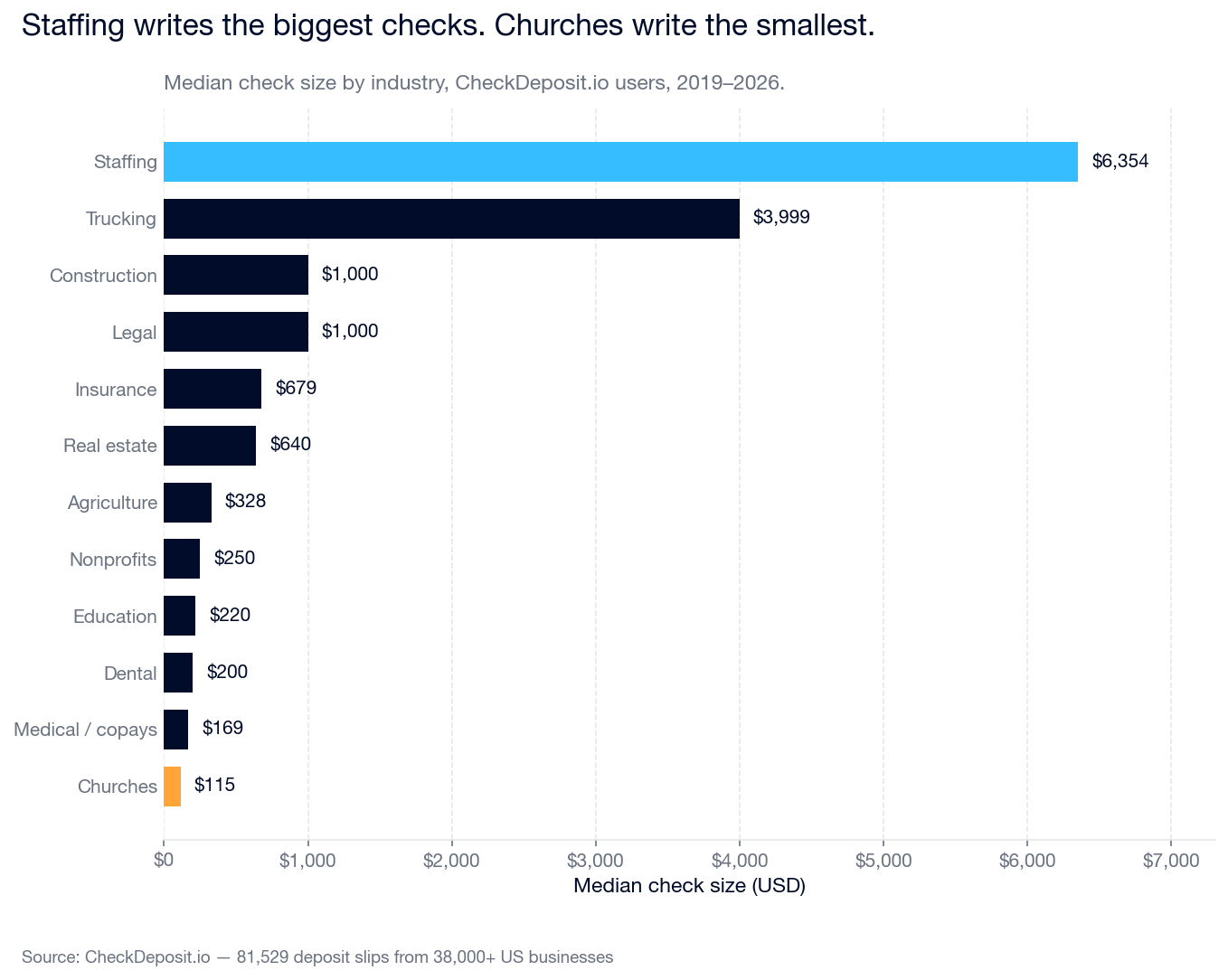

We pulled the company names on every deposit slip and classified them into industries. About a quarter of the slips had company names that matched an obvious industry pattern. Here's what we saw, ranked by share of all deposit slips:

- Medical and healthcare practices (4.3%): Copays, insurance reimbursements. Median check: $169. Small checks, high volume. A typical dental office gets 30 checks a week.

- Construction and trades (3.8%): Progress payments and job deposits. Median check: $1,000. Contractors, HVAC, plumbers, electricians.

- Nonprofits and associations (3.4%): Donations and membership dues. Median $250.

- Real estate (2.7%): Rent, deposits, title work. Median $640.

- Dental and orthodontics (2.2%): Patient payments and insurance. Median $200. Our #1 depositor of all time is an orthodontics practice in East Texas.

- Education and childcare (1.8%): Tuition, field trip checks, lunch money. Median $220.

- Churches (1.5%): Tithes. Median check: $115. The smallest median of any category.

- Legal (1.4%): Retainers, settlements. Median $1,000.

- Trucking and transport (1.1%): Invoices. Median check: $3,999.

- Staffing agencies (0.6%): Payroll and client invoicing. Median check: $6,354. The biggest median of any category.

There's a pattern buried in that list. The smallest checks sit in "every little bit counts" industries: church tithes, medical copays, childcare payments, small donations. The biggest checks sit in B2B invoicing: staffing payroll, trucking invoices, legal settlements, construction progress payments.

This is the Fed paradox with names attached. Staffing agencies and trucking companies are the ones writing the $2,000-plus checks that keep the national dollar total stable. Church tithers and medical copays explain why casual check writing hasn't disappeared entirely. And because our hard-core 44 keep showing up month after month for years, the overall number won't go to zero anytime soon.

Why Checks Aren't Going Anywhere (Yet)

After seven years of watching, the reasons are usually workflow, not preference.

Invoice chains. A staffing agency bills a client for 40 hours of placed workers. The client's accounts payable department cuts a check. The agency deposits it. The chain is paper because the client is paper, and the agency is not going to risk the relationship by demanding ACH. If you're on the writing side of one of those checks, here's how to write a check — the fields banks actually care about and the ones people get wrong.

Insurance reimbursements. Medical practices, dental offices, chiropractors, veterinary clinics all get paid by insurance carriers on paper checks. Every practice we've talked to would happily skip it. The insurance companies are not asking.

Settlements, restitution, donations. Legal settlements are still disbursed by check. Church tithes come in the collection plate, handwritten by people who have written checks since the Nixon administration. Charity donations arrive in the mail because that's how donors were trained to give.

Construction and contractors. Progress payments on a job. Deposits from homeowners. Insurance payouts after a hailstorm. Bonding and retention checks. Paper still rules a big share of the construction payment stack.

The AFP (Association for Financial Professionals) has surveyed corporate treasurers about this for twenty years. Their annual payments survey has consistently shown 30 to 40% of B2B payments are still made by check. Our data shows which 30 to 40%.

Checks are not a dying payment method. They are a specializing one. The industries that still use them have infrastructure, habits, and counterparties that none of them can switch unilaterally.

The 37% Nobody Talks About

One finding from our data doesn't show up in any of the federal check coverage: 37% of the business check depositors on our site operate from residential addresses.

We ran the 100 most recent business deposits through Smarty's address classification API, which flags whether an address is residential or commercial. 37% came back residential. 49% commercial. 14% junk or unknown.

The residential 37% is a specific kind of business. HVAC contractors working from a home office. Trucking LLCs with a home garage. Independent tech consultants. Locksmiths. Small law practices. Donut shops with the books run from a kitchen table.

They are, almost by definition, Schedule C filers. They qualify for the home office deduction. They are the exact overlap between "still gets paid in paper checks" and "still has a shoebox of receipts they haven't sorted."

If you are one of them, reading this from a home office with a stack of checks to deposit on Monday, the irony is that you are probably also leaving several thousand dollars a year on the table at tax time.

So, Are Paper Checks Going Away?

Short answer: federal paper checks, yes. Private-sector paper checks, no.

Longer answer: the checks you write to the IRS and the checks the IRS writes you? Gone. The checks your business gets from customers, vendors, insurance companies, and donors? Very much here. The checks in the collection plate? Here.

The Fed's own data makes the point clearly. Check count will keep drifting down a few percent a year (that's been true for twenty straight years). Total dollar value will not. The average check will keep getting bigger as casual users exit and only the committed ones stay.

$27 trillion a year isn't going anywhere quickly. That's not a prediction; it's what the data has been saying for two decades. In five years we'll still be printing deposit slips for that East Texas orthodontist, that bankers' association, and the other 42 hard-core users.

Plan accordingly.

Frequently Asked Questions

When does the federal paper check phase-out take effect?

It's already in effect. Executive Order 14247 was signed March 25, 2025. The phase-out for IRS tax refunds and most federal disbursements took effect September 30, 2025. The 2026 filing season is the first full year of electronic-only refunds for individual taxpayers.

Will my bank stop accepting paper check deposits?

No. There is no rule or plan changing how commercial banks handle check deposits. Your bank will keep accepting checks, processing them, and posting them to your account. That's independent of the federal government's own payment practices.

Which industries still use paper checks the most?

In our data, medical practices, construction, nonprofits, real estate, dental offices, churches, legal firms, trucking companies, and staffing agencies all still rely on paper checks as a meaningful share of their incoming payments. Staffing agencies write the biggest checks (median $6,354) and churches write the smallest (median $115).

How many paper checks are still written in the US each year?

The 2022 Federal Reserve Payments Study (the most recent, covering 2021 data) reported 11.2 billion checks written in the US, totaling $27.4 trillion in value. That's down from ~42 billion checks in 2000, a 73% collapse in volume. But the dollar value has been basically flat at $25-29 trillion a year for most of that stretch. The reason: average check size has climbed from $945 in 2000 to $2,430 in 2021. Fewer checks, each worth more.

Should I stop accepting checks in my business?

That's a business-by-business call, but our data suggests it's harder than the headlines suggest. If your customers, vendors, or insurance payers are still mailing you checks, moving off them unilaterally is a coordination problem, not a technology one. Our hard-core 44 businesses have each printed 52+ slips a year for years, and they aren't switching because their counterparties aren't switching.

PS from Doug

I'm Doug. I started CheckDeposit.io in 2019 after I left Earth Class Mail. It's been free since day one, and it will stay free. No ads, no signup, no paid tier. If it ever changes, I'll tell you first.

I bought Shoeboxed last November. If you're running a business that still deposits paper checks, there's a reasonable chance you also have a pile of paper receipts you've been meaning to sort. Shoeboxed scans and organizes those for you: receipts, bills, business cards, anything paper. Real humans in North Carolina do the hard part.

There's a risk-free trial if you want to try it. If not, no worries. Print your deposit slip and get back to your Monday.

Doug